What’s the Right Amount to Spend Behind a Franchise QB?

Having been a former athlete, initially, drawing parallels between individuals and policies might not seem quite fitting.

However, after years in the field, one begins to grasp that a player’s contributions in the NFL often translate into a business context.

Undoubtedly, football is a sport that hinges on teamwork. Nevertheless, it’s worth noting that the quarterback position holds an unquestionable level of significance, as many decisions, both within a match and at the organizational level, revolve around the competence of a team’s QB.

Surprisingly, to those viewing the game from the outside, the backup quarterback holds greater importance within an organization than many individuals who partake in the games week after week.

The concept isn’t a groundbreaking revelation or a trendy sports argument. A glance at the compensation levels offers a solid overview of the typical worth attributed to players.

Nonetheless, it’s not a topic that frequently surfaces in discussions beyond the confines of NFL franchises.

Every quarterback scenario within the NFL possesses its distinctive intricacies and conditions.

However, when examining situations where a ‘franchise’ quarterback operates under a contract beyond their rookie deal, optimizing the value of the backup quarterback position is akin to selecting the ideal insurance coverage.

The idea is never to expose your team to unnecessary risks, as the quarterback position is undeniably pivotal.

Yet, you also need to exercise fiscal prudence and avoid overspending or over-allocating resources here, given that the starting QB is typically the highest earner on the team.

Achieving this delicate equilibrium is an art, but the teams that master it gain a substantial advantage in reinforcing other areas of their roster with cost savings.

When the New England Patriots chose to draft Jimmy Garoppolo in the second round at the 62nd pick of the NFL Draft last year, a vocal segment of fans and the media resounded with cries of “Why invest in someone who won’t see playing time?”

It’s a common tendency for those outside the realm of football to disregard, underestimate, or undervalue aspects they don’t witness firsthand, and the backup quarterback role frequently falls into that category.

The genuine concern is how one could contemplate leaving such a critical position vulnerable in a physically demanding sport.

The answer is quite simple: a well-organized team wouldn’t. The NFL operates as a significant business entity, and managing it involves realities beyond managing a roster in a Madden video game.

As it’s prudent to secure insurance for your home, car, and life, investing in your backup quarterback makes sense for comparable reasons.

The value of the protection doesn’t fluctuate based on whether or not you need to utilize it – this is how insurance functions, both in life and in football. The significance of having a reliable and capable backup at the quarterback position cannot be overstated in today’s game.

However, like any other position in a salary cap system, overpaying is akin to squandering resources.

For this discussion, we’re focusing on teams needing a backup quarterback, primarily as an insurance policy for their franchise-leading starter. This narrows the field, excluding roughly half of the NFL teams.

In cases where the starters are less established, the backup role takes on a different dimension.

There often exists genuine competition for the starting position or a willingness to invest more in a seasoned veteran with previous starting experience, as the incumbent starter might not be guaranteed to retain the role.

An illustration of this situation is Matt Cassel’s presence in Buffalo.

For those teams seeking an actual insurance piece, the draft usually emerges as the optimal avenue to explore. The cost is typically justifiable, provided you’re not seeking an insurance policy in the first round.

The asset is too valuable in the initial round to invest in a player who won’t take the field. As you progress beyond the first round, this consideration becomes less critical.

Nevertheless, as you venture past the second and third rounds, the pool of quarterback talent becomes increasingly speculative.

Consequently, selecting a young quarterback in the fourth round or later typically prompts a team to secure an additional veteran backup, at least in the initial year.

Finding the ideal insurance solution at quarterback involves striking a balance and operating best on a sliding scale.

The objective here is to allocate a draft asset to a player who is presently competent enough, negating the necessity for a third quarterback on the roster, with the sooner, the better. This emphasizes the importance of accurately assessing the drafted player’s potential.

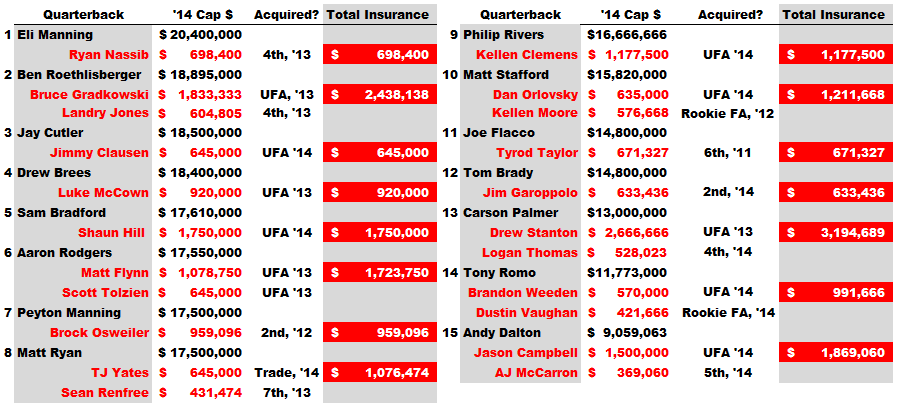

The following graphic provides insight into how teams carrying “franchise quarterback” contracts addressed the backup quarterback role in 2014.

In teams that excel in managing their backup quarterback situation, two recurring strategies stand out:

Successful Draft Picks: These teams have selected a quarterback in the draft who has developed to the extent that they feel comfortable not carrying a third QB. Notable examples include the Giants, Broncos, Patriots, and Baltimore.

Modestly Priced Veterans: Alternatively, they have acquired a veteran quarterback at a reasonable cost, someone they trust enough not to necessitate a third quarterback on the roster. Teams such as St. Louis, New Orleans, and San Diego fall into this category.

For teams without a franchise quarterback, it’s evident that carrying a third quarterback is a wise move.

However, for half of the teams on this list, the ideal situation is to have one of their two backup quarterbacks emerge as a reliable option, enabling them to save both cap dollars and a valuable roster spot. An illustrative case of this is the Pittsburgh Steelers.

Until these teams find a viable solution to their backup quarterback situation, they kick off each season with a disadvantage compared to groups that boast a similarly capable franchise starter and carry only a single backup quarterback.

The precise outcomes of these roster allocations for 2015 will remain uncertain until September when final rosters are solidified.

Excelling in the backup quarterback insurance game may not make you the talk of NFL headlines, but it does provide a substantial advantage in a cap system where every roster spot carries weight.

Nobody aims to be the underinsured property in the neighborhood, but at the same time, being the homeowner in Connecticut with volcano insurance doesn’t exactly represent a prudent choice.

{kind=link}